Self-Directed IRA, Checkbook IRA, Gold IRA, Custodian, Administrator, Disqualified Person, and Prohibited Transactions... What does it all mean?

If you are confused by all of this self directed IRA terminology... You are not alone.

Introduction to Self-Directed IRAs

Individual Retirement Accounts (IRA) also known as Self-Directed IRAs, were created in 1974 to provide a way for Americans to save for their retirement in a tax-efficient manner. Originally the IRA was created to defer taxes on the funds in the retirement account. Much later in 1997, the Roth IRA was created which allowed investors to grow their retirement account tax-free.

These accounts were originally intended for investors to "invest in what they know". This means investing in virtually any investment that they know well enough to make a smart decision about. Since the creation of the Individual Retirement Account (IRA) in 1974, investors have forgotten the original intent of the legislation. More than 90% of the investing public has chosen to invest their retirement into stocks, bonds, and mutual funds.

There is nothing wrong with this strategy if the investor makes a conscious choice. However, many investors are unaware that a choice even exists. Innovative Advisory Group estimates that less than 20% of the investing public is aware of the possibilities available to them with their retirement account. That leaves 80% of the investing public unaware that they can expand their portfolio to include alternative investments that they may be passionate about.

Peter Lynch was famous for his quote, "Invest in what you know". He was referring to the idea that investor should invest in what they know well, rather than in areas where they have less of an expertise. I find that some of the better investments I have seen in my career have come from investors who are experts in that asset. If you are a real estate professional, invest in real estate. If you are a venture capitalist, invest in private companies. If you are a farmer, invest in farmland or livestock. The choices are virtually limitless.

Investing is hard enough. Chose investments where your chances of success are the highest. "Invest in what you know".

Definitions and Terms

The self directed IRA industry, like most of finance, has terms which are not well-defined by conventional standards. Many of these terms are used to mean something that is slightly different than originally intended. This section should provide some clarity on these terms to help you fully utilize our extensive resources.

What is a Self-Directed IRA?

A "self-directed IRA", as stated above has the same meaning as "Individual Retirement Account (IRA)". They technically mean the same thing. All IRAs are self directed. However the term "self-directed IRA" is commonly used to refer to an IRA that has the capability to invest outside the stock market into alternative investments.

All custodians have the capability to invest in stock market investments (stocks, bonds, and mutual funds) and outside of it (alternative investments), however each one can choose what assets they want to provide custody for. If you go to a large discount broker dealer and ask for a self-directed IRA, they might open an account which is limited to stocks, bonds, or mutual funds. If you ask about alternative investments, they might give you a blank stare because they are not aware that those choices are even an option.

This is one of the reasons that it is important to do your research on self-directed IRA custodians and administrators in advance of setting up an account. You want to make sure that the custodian you have chosen, is the best one for your investment needs.

Similar Self Directed IRA Terminology:

There are a few terms similar to "self-directed IRA" that are frequently used to describe the same thing.

- Self-Directed Retirement Account (SDRA): A self-directed retirement account is a term which means any retirement account that is "self-directed". This includes self-directed IRAs, 401(k)s, 403(b)s, and other group plans.

- SDIRA: This is shorthand for "self directed IRA"

- Self-directed 401(k): Typically this term refers to a 401(k) plan which allows the plan participants to chose their own options from an expanded list (e.g. 5,000 choices vs the typical 5-25 mutual funds). 401(k) plans have different rules than IRAs, you can read more about self-directed 401(k)

pl ans here. - SD401k: This is shorthand for self-directed 401(k)

What is an Alternative Investment?

Alternative Investments is a term which does not have a clearly defined and broadly accepted meaning. Depending on who you ask, it can be used to mean different things. If you talk to someone who works at a traditional financial firm, they might assume you mean that alternative investments refer to hedge funds. More recently the term has been expanded to other assets such as private equity funds, managed futures, venture capital, MLPs, BDCs, or structured products.

If you are speaking with someone who understands self-directed IRAs, they would assume that you mean alternative investments refers to any investment outside the publicly-traded stock and bond markets. Examples of these types of alternative investments might be real estate, tax liens, private notes, trust deeds, farmland, water rights, oil & gas LPs, private company stock, franchises, precious metals, structured settlements, and more.

The best way to think about alternative investments is that every person's perspective is different. If you only have experience with mutual funds, then structured settlements might be alternative, if you only know real estate, then tech companies might be alternative. Regardless of how you feel about the term, we will be using the term in our reports to refer to investment assets that outside the stock and bond markets.

If you want more examples of alternative investments, you can request our Bonus Report. This report will provide you with 75 different alternative investments that you can consider for your investment portfolio if you are looking to invest outside the stock market...

What is a Self-Directed IRA Custodian?

A Self Directed IRA Custodian is a company that provides custody and safekeeping of investments held in your self-directed IRA. Using a "qualified custodian" is part of the requirements of having a self-directed IRA. In addition to providing custody, many of these companies also provide administrative services such as tax reporting, providing periodic statements, processing documentation, processing annual valuations, fund accounting, maintaining cash bank accounts, foreign exchange transactions, arranging settlement of any purchases and sales of securities and currency, provide legal, compliance and tax support services.

Custodians are chartered, licensed, and regulated by governmental agencies. Some of these regulatory agencies include the Office of the Comptroller of the Currency(OCC), Office of Thrift Supervision (OTC), and state regulatory agencies. In many cases bank and trust companies would also be considered custodians under this definition. If you are unsure if the custodian you are considering is a qualified custodian, you can contact their regulator for more information. We have provided the names of the agency that regulates each of these firms in our company reports.

While there are many qualified custodians to choose from, we have only included the ones that specialize in self-directed IRAs holding alternative investments in our resources. Click the button below to see the list of self-directed IRA custodians.

What is a Self-Directed IRA Administrator?

A Self-Directed IRA Administrator or Third-Party Administrator (TPA) is a firm that provides administrative services to custodians pertaining to

It is important to note that you have a choice of whether to use a

Some administrators will mask who the custodian is that they are using, making it hard to know who is ultimately providing custody for your accounts. We have provided that information for you in our reports, but if you ever have questions or concerns about this, please contact the administrator to ask. They should tell you. If they won't tell you who is providing custody of your accounts, then you should be concerned. You may want to explore other options if the firm is not completely transparent.

We have created the IAG Transparency Index for investors who want to know the level of transparency the custodian or administrator is willing to provide. It is not the only factor in making a decision, but it is an important one to consider.

What is a Self Directed IRA Facilitator?

A Self-Directed IRA Facilitator is a person or company that provides services to self-directed IRA or 401k account holders. Examples of these services are: providing you with 401k plan documents, assisting you in the creation of a LLC, and assisting you with IRA account paperwork. There are licensed and unlicensed facilitators.

Licensed Facilitators are professionals who are licensed and regulated by a governmental agency. These professionals can help their clients with the setup and processing of self-directed IRA account documentation. If you get stuck with your self-directed IRA, these professionals may be able to provide you with the assistance you need. Examples of licensed facilitators: attorneys, accountants, and financial advisors. Not all of these professionals have a proficiency or specialization in the area of self-directed IRAs, so you should ask them about their knowledge and experience. This is a Complete List of Licensed Advisors for Self-Directed IRAs

Unlicensed Facilitators are individuals or companies who provide services to self-directed IRA account holders. These individuals or companies are not licensed professionals and do not have any regulatory oversight or supervision. You should be cautious about the services they provide. While it may seem as if they are offering legal or financial advice, you should not rely on them for this type of expertise.

Some of these companies have an attorney on staff to provide legal advice. If this is one of their services, you should get the person's name and verify they are licensed to practice law. Due to the lack of regulatory oversight of self-directed IRA facilitators, it is easy to find fly-by-night companies which may be less than reputable. A number of these facilitators also sell investment products. Unlicensed facilitators can also be referred to as coordinators.

Important Note: Many self-directed IRA facilitators do not distinguish themselves as licensed or unlicensed facilitators. Most of them are unlicensed. Since these people are not licensed or regulated, it may not be clear to you if you are paying them to be helpful, and or if they are being compensated by promoting their own products or investments. Due to this lack of supervision from a regulatory authority, be careful if you engage one of these people to help you.

What is a Self Directed IRA Coordinator?

Self Directed IRA Coordinators are people who help to coordinate a portion of the process of setting up a self-directed IRA or self-directed 401k. This may include: using their “approved” plan documents, creating LLCs, account forms, or other specific duty. While coordinators may be helpful, they are not essential to the process of setting up a self-directed IRA and investing with it.

This is a relatively new category in the Self-Directed IRA industry. Coordinators were formerly called (unlicensed) facilitators. Many of them still refer to themselves as facilitators. However there is a big distinction between someone who is a licensed professional, helping to facilitate the process of setting up and maintaining a self-directed IRA, and someone who is not. This clarification in the definition above should help give prospective investors a better understanding of the person they are working with.

What is an Investment Sponsor?

An Investment Sponsor is a person or company that is sponsoring or soliciting interest in an investment that they personally benefit from. An example of this is a company which sells real estate to investors as ready-to-invest investments, REITs, or pooled funds. Another example of an investment sponsor is a real estate investor who uses hard money to rehabilitate properties and solicits investors to loan him money so he can complete his project. In this case, he would be sponsoring his own investment

Important Note: The primary motivation of the investment sponsor is to sell their product or raise money to invest in a certain project. In some cases, these investment sponsors offer to assist investors in order to facilitate the setup and investment of the investor's IRA or 401(k) into the sponsored investment. Do not consider this as legal or financial advice. If you need advice, you should seek the counsel of a licensed attorney, accountant or financial advisor.

What is a Prohibited Transaction?

A Prohibited Transaction can be described as an improper use of your IRA account by a disqualified person. The IRS defined a prohibited transaction as,

"A prohibited transaction is a transaction between a plan and a disqualified person that is prohibited by law... If you are a disqualified person who takes part in a prohibited transaction, you must pay a tax."

"A prohibited transaction is a transaction between a plan and a disqualified person that is prohibited by law..."

If you create a prohibited transaction with your IRA or 401k, you could have adverse tax implications in your retirement account.

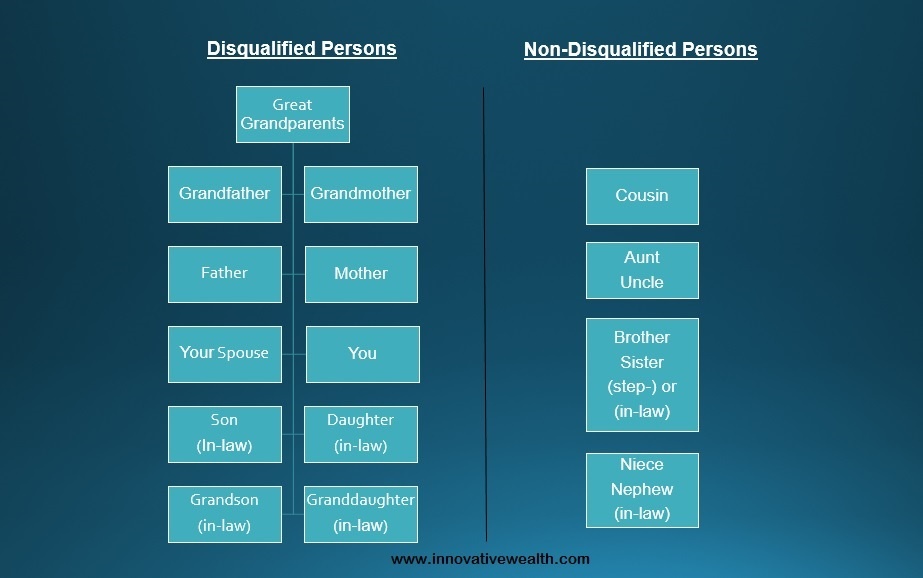

What is a Disqualified Person?

A Disqualified Person is a person who is prohibited from transacting directly or indirectly with an IRA [as described in IRC 4975(c)(1) ].

What is a Checkbook IRA

A Checkbook IRA is a marketing term used by individuals and companies looking to promote the idea of the "single-member LLC". The single-member LLC and checkbook IRA the same thing. Single-member LLCs are allowed as an asset which could be held in a self-directed IRA.

The checkbook IRA works as follows:

- The IRA would be the owner of the LLC.

- Once the LLC is set up, a bank account could be established in the name of the LLC.

- The IRA invests in the LLC, and the funds from the IRA get deposited into the bank account.

- The "checkbook" from the new bank account could be used to invest in virtually any investment.

While this process is allowed in accordance with the IRC, it can be dangerous if the IRA account owner is not careful. This type of transaction should not be managed by an inexperienced self-directed IRA investor. Many self-directed IRA custodians will not allow single-member LLCs to be held in custody at their firm. This is primarily due to the potential liability these types of assets can cause. If you are not familiar with how a checkbook IRA works, please seek the counsel of a licensed professional.

What is a Gold IRA?

The Gold IRA is a marketing term used by individual and companies looking to promote the idea of investors buying physical precious metals to be held in their self-directed IRA. There is no special IRA that needs to be created for investors to buy gold and silver as an investment in their IRA. Any IRA is able to do this for you, however only certain self-directed IRA custodians and administrators will permit this asset to be held at their firm.

There are many subtle nuances about how this process works. You will need to find a custodian or administrator that will allow gold to be held in your IRA, then you will have to find a depository to store the gold, then you will need to find a coin dealer to buy the gold from. If you want to know the rules for the "Gold IRA" you can read about it here. This article will describe the exact specifications of the gold allowed by the Internal Revenue Code.

What is a Real Estate IRA?

The Real Estate IRA is another marketing term used to describe an IRA that is invested in real estate properties. As stated above with the gold IRA and checkbook IRA, there is nothing different about this type of IRA other than the asset being held in it. As long as the self-directed IRA custodian or administrator allows this asset to be held at their firm, you should easily be able to invest in real estate with your existing self-directed IRA. If you don;t already have a self-directed IRA, you can learn more about investing you IRA into real estate here.

What is a Self-Directed 401k?

The Self Directed 401k is virtually the same as the self-directed IRA. However, there are a few subtle differences. The self-directed IRA is an Individual Retirement Account (IRA), whereas the self-directed 401k is a retirement account which is sponsored by a company. The company that sponsors the 401k plan may be a company with just a single employee (you) or a company with 100,000 employees. The rules are the generally the same.

The term "self-directed 401k" is used to describe a 401k account which can be directed by the plan participant. This means in a company of just one employee, you can direct the investment decisions. If the company has 100,000 employees, it will be up to the company to decide what investment choices the company will allow their employees. Some companies allow a "self-directed" option where the employee can open up a "brokerage" account to self-direct the 401k account. These choices are at the discretion of the sponsor of the plan (the company).

Read more on this page if you want to learn more about the self directed 401k.

Additional Self-Directed IRA Resources:

- The Ultimate List of Self Directed IRA Custodians and Administrators

- 9 Common Mistakes Investors Make with Self Directed IRAs

- The Quick Start Guide to Self Directed IRAs

- 28 Questions You Should Ask Your Self Directed IRA Custodian

- Self Directed IRA Rules, Regulations, and Resources

- The Complete List of Advisors For Your Self Directed IRA

- Self Directed IRA Frequent Asked Questions (FAQ)

- The Ultimate Due Diligence Guide of Self Directed IRA Custodians and Administrators