| Index | Value | 1mo change | 1yr change | 5yr change | Inflation Score |

|---|---|---|---|---|---|

| Economic Inflation | |||||

| Consumer Price Index (CPI) | 237.34 | -0.21% | 0.50% | 8.47% | 2 |

| Producer Price Index (PPI) | 185.90 | -0.96% | -7.47% | -0.96% | 1 |

| 1 Yr Treasury Bill Yield | 0.48% | 0.22 | 0.35 | 0.23 | 2 |

| 10 Yr Treasury Note Yield | 2.15% | -0.02 | -0.07 | -1.14 | 2 |

| Real Interest Rate | -0.02% | -0.11 | 1.17 | 0.87 | 3 |

| US 10 yr TIPS | 0.58% | -0.07 | 0.15 | -0.46 | 2 |

| Capacity utilization | 77.00 | -0.65% | -2.53% | 2.53% | 2 |

| Industrial Production Index | 106.53 | -0.56% | -1.17% | 11.53% | 3 |

| Personal Consumption Expenditure Index | 12,393.5 | 0.12% | 2.92% | 19.82% | 3 |

| Rogers International Commodity Index | 2130.79 | -7.59% | -22.49% | -39.29% | 1 |

| SSA COLA | 0.00% | 0.00% | 3 | ||

| Median Income | $53.657.00 | 0.13% | 7.79% | 3 | |

| Real Median Income | $53,657.00 | -1.48% | -2.31% | 3 | |

| Consumer Interest in Inflation | Stable | 3 | |||

| IAG Inflation Composite | Strong Deflation | 1 | |||

| IAG Online Price Index | Slight Deflation | 2 | |||

| US GDP | 18034.80 | 0.68% | 2.93% | 19.77% | 4 |

| S&P 500 | 2102.63 | -0.07% | 2.35% | 69.36% | 4 |

| Market Cap to GDP | 115.90% | 120.10% | 81.80% | 4 | |

| Corporate Debt as % of Equity | 39.00% | 3.80 | 5.10 | -8.20 | 1 |

| US Population | 322,536 | 0.06% | 0.73% | 4.12% | 2 |

| IAG Economic Inflation Index* | Slight Deflation | 2 | |||

| Housing Inflation | |||||

| Median Home price | 219,600.00 | -1.04% | 5.83% | 28.72% | 4 |

| 30Yr Mortgage Rate | 3.94% | 0.14 | -0.06 | -0.36 | 4 |

| Housing affordability | 166.30 | 1.59% | -1.36% | 4 | |

| US Median Rent | 803.00 | 6.22% | 15.71% | 4 | |

| IAG Housing Inflation Index* | Mild Inflation | 4 | |||

| Monetary Inflation | |||||

| US Govt debt held by Fed (B) | 2,797.50 | 0.15% | 7.00% | 260.18% | 1 |

| US Debt as a % of GDP (B) | 100.48% | -0.85% | -1.25% | 10.41% | 2 |

| M2 Money Stock (B) | 12,295.80 | 0.97% | 6.20% | 40.56% | 4 |

| Monetary Base (B) | 4,029.27 | -1.14% | 4.63% | 102.19% | 3 |

| Outstanding US Gov’t Debt (B) | 18,150,618 | -0.01% | 1.83% | 33.84% | 4 |

| Velocity of Money [M2] | 1.49 | -0.67% | -2.61% | -14.51% | 2 |

| US Trade Balance | -43,891.00 | -7.54% | -2.66% | -9.73% | 1 |

| Big Mac Index | Expensive | 1 | |||

| US Dollar | 100.25 | 3.54% | 13.44% | 33.94% | 1 |

| IAG Monetary Inflation Index* | Mild Deflation | 2 | |||

| Energy | |||||

| Electricity (cents / KW hour) | 13.60 | 5.18% | 5.02% | 4 | |

| Coal (CAPP) | 43.50 | -11.22% | -22.74% | -41.61% | 1 |

| Oil | 41.73 | -10.12% | -36.77% | -50.12% | 1 |

| Natural Gas | 2.23 | -1.76% | -43.90% | -46.85% | 1 |

| Gasoline | 1.32 | -4.01% | -28.15% | -39.81% | 1 |

| IAG Energy Inflation Index* | Strong Deflation | 1 | |||

| Food and Essentials | |||||

| Wheat | 474.00 | -8.85% | -17.99% | -31.60% | 1 |

| Corn | 372.25 | -2.36% | -3.56% | -31.57% | 2 |

| Soybeans | 887.50 | 0.00% | -12.19% | -28.79% | 1 |

| Orange Juice | 142.20 | 6.16% | -4.47% | -4.69% | 3 |

| Sugar | 14.85 | 2.27% | -4.32% | -45.96% | 2 |

| Live Cattle | 141.13 | 0.00% | -16.44% | 32.39% | 1 |

| Cocoa | 3344.00 | 2.83% | 17.29% | 18.29% | 5 |

| Coffee | 120.00 | -0.83% | -35.69% | -40.40% | 1 |

| Cotton | 62.74 | -0.95% | 4.65% | -46.53% | 3 |

| Stamps | $0.49 | 0.00% | 6.52% | 11.36% | 4 |

| CRB Foodstuffs Index | 363.64 | -0.62% | -7.28% | -10.81% | 2 |

| IAG Food and Essentials Inflation Index* | Mild Deflation | 2 | |||

| Construction and Manufacturing | |||||

| Copper | 2.05 | -11.36% | -28.03% | -45.37% | 1 |

| Lumber | 246.80 | -2.72% | -25.05% | -1.67% | 1 |

| Aluminum | 0.67 | 1.52% | -19.28% | -37.38% | 1 |

| CRB Raw Industrials | 400.73 | -3.11% | -20.39% | -27.98% | 1 |

| Total Construction Spending (M) | 1,107,381.00 | 0.98% | 13.05% | 35.40% | 5 |

| ISM Manufacturing Index | 48.6 | -2.99% | -15.63% | -15.63% | 1 |

| IAG Construction & Manufacturing Index* | Strong Deflation | 1 | |||

| Precious Metals | |||||

| Gold | 1,064.60 | -6.70% | -8.18% | -23.28% | 2 |

| Silver | 14.01 | -9.84% | -8.99% | -50.24% | 2 |

| IAG Precious Metals Inflation Index* | Mild Deflation | 2 | |||

| Innovative Advisory Group Index | |||||

| IAG Inflation Index Composite* | Mild/Strong Deflation | 1 / 2 | |||

* If you would like a description of terms, calculations, or concepts, please visit our Inflation monitor page to get additional supporting information. We will continually add to this page to provide supporting information.

* Our Inflation Score is based on a proprietary algorithm, which is meant to describe the respective category by a simple number. The scores range from 1-5. One (1) being the most deflationary. Five (5) being the most inflationary. These scores are meant to simplify each item and allow someone to quickly scan each item or section to see the degree of which inflation or deflation is present.

* We have also added our own indexes to each category to make it even easier for readers to receive a summary of information.

Inflation Monitor Summary – Composite Ranking

* The Inflation Equilibrium is a quick summary for the whole data series of the inflation monitor. If you don’t like statistics, this is the chart for you.

Inflation Monitor – December 2015 – Introduction

This is the last issue of 2015. I hope you are enjoying the holidays and getting ready to bring in the new year. While this is a joyous time of the year. It should be used to reflect on the past year and what surprises are to come in the next 12 months. While no one can know the future, we can look for signs that things are not quite right. These are what I would call new potential risks to the equilibrium of the global financial markets.

Here is a good summary of the economy and markets as they exist today. It is quoted from the introductory paragraph of Michael Lewitt’s, The Credit Strategist:

Commodity prices are plunging, the dollar is powering higher, the yield curve is flattening, Obama Care is collapsing, global trade is plummeting and terrorism is spreading across the globe. The high yield credit markets are sending distress signals and 10-year swap spreads are negative. Energy companies are going out of business faster than you can say “frack” and trillions of dollars of European bonds are again trading at negative interest rates. The world is drowning in more than $200 trillion of debt that can never be repaid while European and Japanese central bankers promise to print more money and the Federal Reserve is being dragged kicking-and-screaming into raising interest rates by a paltry 25 basis points. Accurate pricing signals in the markets are distorted by over-regulation, monetary policy overreach and group think. Hedge funds are hemorrhaging and investors, desperate to generate any kind of nominal return on their capital, continue to ignore the concept of risk-adjusted returns. Some market strategists believe this is a positive environment for risk assets; I am not among them.

Michael has a way with words. I don’t think I could summarize the state of the global markets better than he did in such a small amount of space. That being said, let’s dive into some charts and take a look at the past year to see what we can dig up for next year’s outlook.

In case you were not aware, the high-yield bond market, which tends to be a leading indicator for the stock market, has been taken out to the woodshed. There are no words… oh wait there are. Here are some views of other experts and market observers.

Here is a more recent quote from Jeffrey Gundlach, Doubleline Capital

“We’re looking at some real carnage in the junk-bond market. This is a little bit disconcerting that we’re talking about raising interest rates with the credit markets in corporate credit absolutely tanking. They’re falling apart.”

The High yield bond market has been getting really ugly lately. I hope you don’t still own any. This issue has been observed by a number of investors for the past year. There has been plenty of time to prepare for the high yield bond market problems. If you are surprised by any of this, then you have not been paying attention.

Here is a news clip from the WSJ last week, “Third Avenue Focused Credit Fund takes rare step, seeking an orderly liquidation as junk-bond market swoons“. As of Dec 11th close HYG (high yield ETF) closed down -11.25% for the YTD. While an index down 11.25% for the year in of itself is not a big deal. The fact that this rout in high yield bonds has caused the first high yield bond fund to freeze future redemptions is a problem. There will be some great opportunities there, as long as you have not lost your shirt before that.

Stay safe, and remember cash is king. And it rules when “deflation” is the word of the day. If you don’t know how deflation works, now would be a good time to learn.

I hope you enjoy this month’s Inflation Monitor – December 2015.

Kirk Chisholm

As always, please contact me with any questions or to send your feedback. Thank you for reading.

Join our email list to receive the Inflation Monitor sent directly to your inbox.

![]()

Charts of the Month

Leading Indicators

Dr. Copper

Dr. Copper is still weak. the downtrend is continuing. At some point, there will be a tremendous opportunity to buy this essential metal, but right now investors of copper are running for the exits. The beginning of next year might send a rise in prices (briefly).

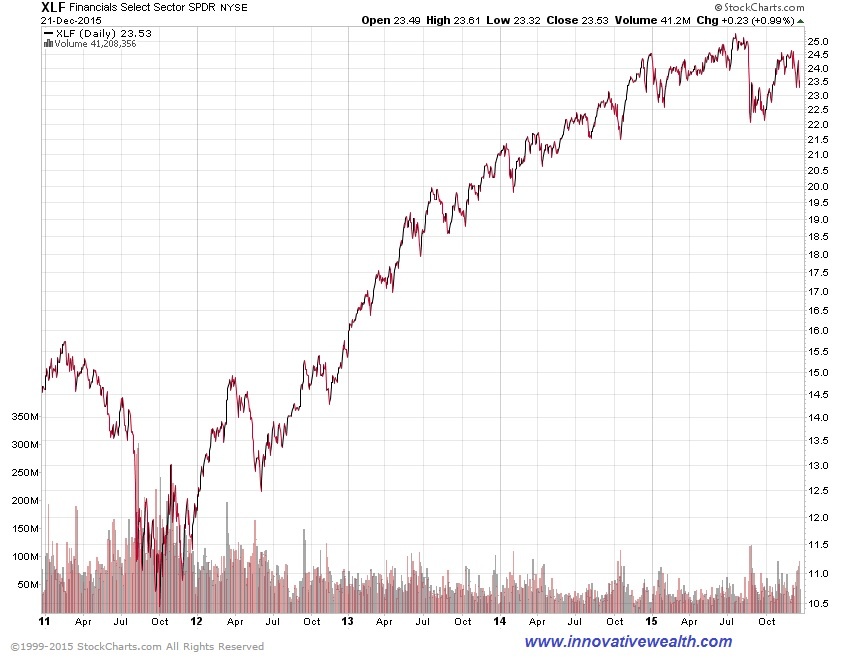

Financials

Financial are holding steady. Fed decided to raise interest rates in December, that could help the financials. However, the yield curve is still flat and getting flatter with the short end of the curve rising and the longer end not rising. So the “help” might be insignificant with all the penalties, fee, fines, etc they are paying.

Consumer Price Ratio (CPI)

The CPI is flat for the year. If you have read this Inflation Monitor report for the last 12 months you will know that strong deflationary forces are here to stay. The Fed does not want deflation in the US, but can they stop it? We will find out soon enough what tricks they have up their sleeve.

Producer Price Index (PPI)

The Producer Price Index is continuing to have a rough time this year. The declining PPI might be a reflection of the new economic conditions of producers and manufacturing with a high value of the US Dollar. This makes it harder for US companies to export goods since they will be about 20% more expensive from where they were last year.

US Velocity of Money M2

This is a clear sign that inflation is not around the corner. Don’t bother even looking for it. Once again deflation is the active trend. How low can this go… No santa clause rally on this chart.

ISM Manufacturing

Gas Prices in Massachusetts

“We keep thinking that lower energy prices are somehow good for the economy. That can’t be, because energy prices or commodity prices in general don’t drive economic growth. Economic growth drives commodity prices.”

~Stephen Schork

Gas prices have dropped to more reasonable levels, but I think we could still drop lower. Oil prices have already broken below $35 earlier this month, I suspect they will continue lower. The world seems to be running out of oil storage. Oil producers seem intent to continue producing oil. What happens when they run out of storage? I guess if history is any lesson, now is the time the US government will announce that they will sell most of the US oil reserves. Nothing like timing the bottom of the market. They also tend to buy more when oil prices are high too. A great contrarian indicator if I ever saw one.

Gas Prices in the US

Currency Relative Valuations to Gold

Gold is priced in the currency you use every day. If you live in the European Union, you use Euros, if you live in Japan, you use Yen, and if you live in the US you use US dollars. Each of these currencies is used to buy gold in their respective countries, so we look at gold priced in each country to see how people value it in their own currency. This can tell us a lot about the demand for gold inside and outside the US.

Gold prices are they strong or weak?

Gold Priced in Euros

Gold Priced in Yen

Gold Priced in Canadian Dollars

Gold Priced in Australian Dollars

Bonds

TED Spread

A surge in the Ted Spread means a lack of trust in financial institutions. This is not a good trend, although it is off low. It is far off the 2008 highs of 4.6, but the upward trend is not a good sign, since it is confirming many other indicators.

10 year vs. 2 year Treasury Spread

The flattening (or inverting) of the yield curve is not good for banks and also typically shows signs on a recession. It is probably one of the best indicators of a recession we have, yet no one knows the status since interest rates are stuck at zero… sorry 0.25% -0.50%

Treasury vs Corp Bond Spread

The spread between 30-year treasuries and corporate bonds is relatively high, as it can be in times of market distress. It will be interesting to see how this plays out as interest rates start to rise… assuming they ever do.

High Yield Bonds (Junk Bonds)

High yield bonds have had a good run of very low default rates. 2014 was around 1%. During recessions, these default rates tend to climb up to around 10% (1991, 2001, 2002, and 2009). This is fine unless you are getting 5% on your high yield bond income. In that case, you would net -5% a year. I’ll bet that is not quite what you had in mind when you were looking for income.

It is important to point out that high-yield bonds are going through a period of turmoil. Recently 3 high yield funds have closed their doors due to investors pulling their money out. You can read about this turmoil and the blueprint for financial contagion in my 2015 year end recap.

High Yield bond spread helps point out areas of fear in the high yield bond market.

A strong correlation between S&P 500 and high yield bond spreads

Inflation Dashboard

I like this view because it give more of a visual perspective of the data presented above.

{kind=link}

{kind=link}

All Kinds of Debt

“High debt levels, whether in the public or private sector, have historically placed a drag on growth and raised the risk of financial crises that spark deep economic recessions.”

~The McKinsey Institute

Corporate Debt as a Percentage of Equity

Public Sector vs Private Sector

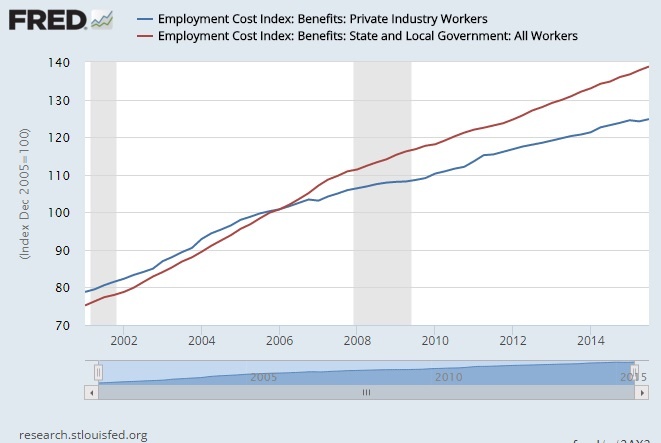

Public Sector vs Private Sector Benefits

I thought one of the reasons for working for the government was the better benefits which make up for the lower pay. Apparently it is just better benefits.

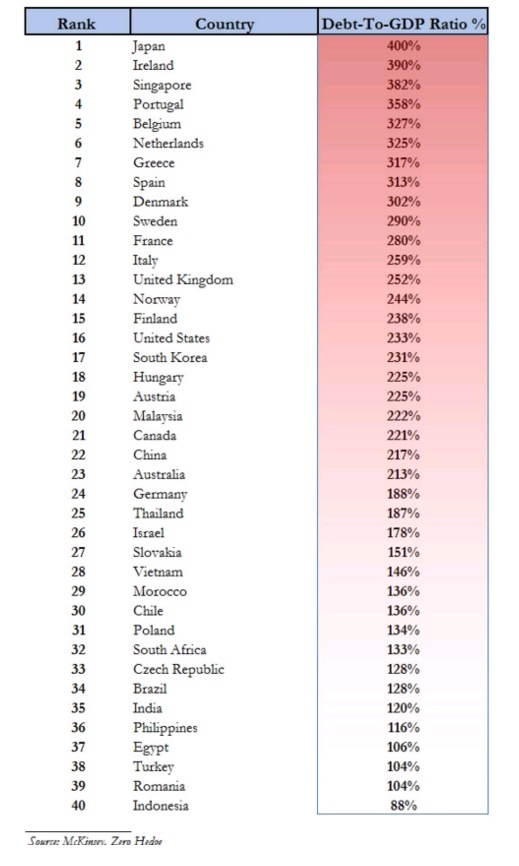

Global Debt to GDP

If the high debt-to-GDP doesn’t scare you… it should.

Despite the high amounts of debt in the global economy, not everyone is leveraging up. The US has made some dramatic improvements in the household sector. However, a number of countries are leveraging up in a period where they are already over 100% debt to GDP. The PIIGS and Singapore still seem to be in trouble.

This is a cleaner version of the debt to GDP.

Canada and Oil

Canada’s oil sector amounts to about 10% of its GDP and 25% of its exports, almost all of which go to the U.S.

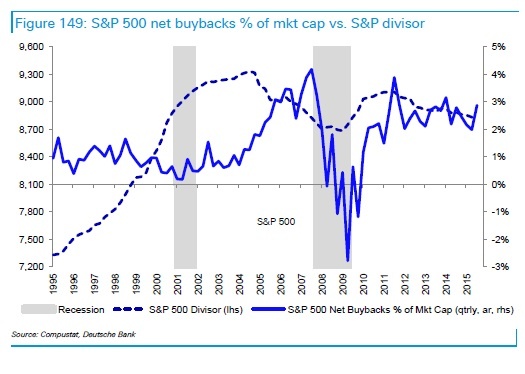

Corporate share buybacks

I know there is an opinion out there that share buybacks are manipulating corporate earnings. I say yes they are, and yes they should. The job of the company is to provide value to its shareholders. If buying back shares is the best way to provide value to the shareholders, then by all means, do it. This strategy was detailed in the book, The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success. The problem is not that share buybacks is wrong or manipulative, it is that many CEOs endorse the strategy to grow earnings rather than buying their shares because they are cheap. CEOs who can allocate capital in a smart way, are rare gems and should be followed.

DB put out a nice 2016 outlook recently, they predict that since 2012, buybacks contributed to 20% of EPS growth in the S&P 500. They also predict that it will contribute to ~1% EPS growth in 2016.

The first chart shows how much of S&P 500 EPS growth comes from buybacks. Depending on what happens in the 4th Quarter, it could be all of it.

This second chart shows that CEOs do a poor job of capital allocation during times of distress. Smart managers should have been buying their shares hand-over-fist during the 2008-2010 period. But they didn’t. I highly recommend the Outsiders book if you are interested in well-run companies.

This last one breaks down the buybacks and dividends by sector to show the total shareholder yield.

Q Ratio

I hope you enjoyed this month’s Inflation Monitor. See you next month.

Cheers,

![]()

Kirk Chisholm

The IAG Inflation Monitor – Subscription Service

We are initially publishing this Inflation Monitor as a free service to anyone who wishes to read it. We do not always expect this to be the case. Due to the high demand for us to publish this service from a wide variety of people who subscribe, we do at some point in the next 12 months expect to charge for this service. Our commitment to our wealth management clients is to always provide complimentary access to our research. If you would like to discuss becoming a wealth management client, feel free to contact us.

If you would like to automatically receive the Inflation Monitor in your email inbox each month, click here to join our free subscription service.

![]()

Sources:

- Federal Reserve – St. Louis

- U.S. Energy Information Administration

- U.S. Post Office

- TD Ameritrade

- National Association of Realtors

- The Economist

- The Commodity Research Bureau

- Gurufocus.com

- Stockcharts.com

- GasBuddy

- McKinsey

* IAG index calculations are based on publicly available information.

** IAG Price Composite indexes are based on publicly available information.

About Innovative Advisory Group: Innovative Advisory Group, LLC (IAG), an independent Registered Investment Advisory Firm, is bringing innovation to the wealth management industry by combining both traditional and alternative investments. IAG is unique in that we have an extensive understanding of the regulatory and financial considerations involved with self directed IRAs and other retirement accounts. IAG advises clients on traditional investments, such as stocks, bonds, and mutual funds, as well as advising clients on alternative investments. IAG has a value-oriented approach to investing, which integrates specialized investment experience with extensive resources.

For more information, you can visit: innovativewealth.com

About the author: Kirk Chisholm is a Wealth Manager and Principal at Innovative Advisory Group. His roles at IAG are co-chair of the Investment Committee and Head of the Traditional Investment Risk Management Group. His background and areas of focus are portfolio management and investment analysis in both the traditional and non-traditional investment markets. He received a BA degree in Economics from Trinity College in Hartford, CT.

Disclaimer: This article is intended solely for informational purposes only, and in no manner intended to solicit any product or service. The opinions in this article are exclusively of the author(s) and may or may not reflect all those who are employed, either directly or indirectly or affiliated with Innovative Advisory Group, LLC.