“Wealth is the ability to fully experience life.”

– Henry David Thoreau

“Wealth” — can be defined as assets or resources which are in excess of present or future expected expenses. A more simple explanation is that wealth is made up of assets which exceed what will be needed for this generation, and could be passed onto the next one. Even though wealthy families may not need their wealth for this generation, proper stewardship is required to make sure those assets will last for future generations.

The main considerations in protecting wealth for future generations of wealthy families are that the assets must be sustainable over several generations, resistant to inflation, and resistant to political and economic turmoil. It is possible to invest in certain assets that can fortify your wealth against some of these external risks. However, there is a much greater risk of future generations not being good stewards of sustainable wealth. Whether you are the first generation to create generational wealth, or whether you are researching how to sustain the wealth you have inherited, this list will give you some guidance.

Top 10 ways to make sure your assets endure the test of time

1. Proper Financial Planning

It is no coincidence that this is first on the list. It doesn’t matter how well the wealth is grown in one generation, without proper planning the wealth could easily be lost in future generations to taxes, high professional fees, poor investments, and unprepared recipients of the wealth.

It is important to start with a road map that plans the direction of the future sustainability of the family’s wealth. This road map should clearly outline how the wealth should be managed and invested for future generations. It should also incorporate tax planning strategies to minimize the effect that taxes have on wealth over generations. You should seek a financial planning professional who specializes in your area of focus as well as one who has experience working with your level of wealth. For example, if your family has $50 Million in assets, you should seek an estate planning attorney who has a lot of experience with these amounts and the appropriate strategies.

2. Investment Education

It is also not a coincidence that this is second on the list. Education is extremely important if the family wants their wealth to last multiple generations. While higher education in the form of college and graduate degrees is important, it is more important to have education in the form of experience and wisdom passed down from those family members who have either earned the wealth or have experience managing it successfully.

Families like the Rockefellers have been able to build enormous wealth and sustain it for multiple generations in large part through the education of family members pertaining to the family’s wealth. Nelson Rockefeller frequently told how his father gave each of his children an allowance of 25 cents, but if they wanted more money they had to earn it by working. He also required that they account for where all their money went. These types of lessons are what is important to pass down to the next generation.

While it is important for every family to teach their children about money and wealth, the burden of large amounts of wealth can be difficult for an inexperienced family member to manage on their own. There are many examples of professional athletes, lottery winners, and winners of large legal settlements receiving large amounts of wealth with little experience, and then subsequently losing it due to lack of experience in managing it.

If no one in the family has the skill set to educate the other family members, then professional advice should be sought to help in this education. Financial advisors, attorneys, and tax professionals are an important part of this process. Each should be sought out for a skill set that matches the family’s needs.

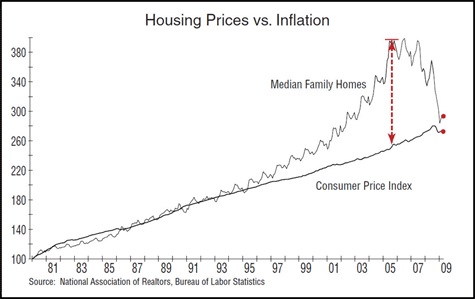

3. Real Estate

For centuries people have been using real estate to protect and grow wealth. This asset class is one of the better time-tested investments for generational wealth. Real estate can be in the form of land, residential housing, air space, mineral, water or fishing rights, commercial or industrial properties. What makes real estate such a special asset class is that it has all the markers for a generational wealth asset. Real estate is a great hedge against inflation, it provides income, it is very suited for generational wealth transfer due to favorable US tax laws, it is an asset which will always have a demand for it since people need somewhere to live, favorable income tax treatment, it is resistant to political and economic turmoil, and can be leveraged to suit risk tolerance of the family.

4. Precious Metals (Gold & Silver)

Precious metals have been considered money and a storage of wealth for over 2000 years.  Gold and silver are an integrated part of many cultures around the world as a form of money or storage of wealth. While gold and silver have technically become delinked from all paper or fiat currencies over the past few decades, they are still perceived as money by many people regardless of how their respective governments see them.

Gold and silver are an integrated part of many cultures around the world as a form of money or storage of wealth. While gold and silver have technically become delinked from all paper or fiat currencies over the past few decades, they are still perceived as money by many people regardless of how their respective governments see them.

Over centuries gold and silver have been seen as the best forms of money for the following reasons: it is divisible, durable, consistent, convenient, and has a value in of itself. Regardless of whether gold and silver are actually used as money in day-to-day transactions for goods and services, they are seen to have one of the best characteristics of a store of wealth or money, an asset that retains its purchasing power over long periods of time.

While it is best not to blindly follow what other people do, no matter how wealthy they are, it should be noted how many wealthy families own gold as a storage of wealth. Regardless of the current public opinion of gold and silver, many Swiss vaults are lined with gold bullion from wealthy families who value gold as permanent storage of wealth.

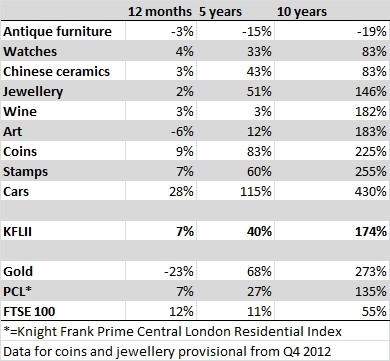

5. Collectibles

A collectible is an item that either currently has value (wealth preservation) as a collectible or will have greater future value (speculation) as a collectible item. The types of collectibles are almost limitless, but some examples of these items are paintings, artwork, stamps, vintage wines, coins, rugs, or cars. Most of the collectibles bought by wealthy families are already considered valuable, so it is not necessarily speculation of future value. Since wealthy families already have a large amount of wealth, their goal is not to grow it, but rather to keep it, so preservation of wealth is more important to them than speculation.

Collectibles are a favored asset class by wealthy families. The items are typically purchased for some personal enjoyment, but also accomplish the ability to be a hedge against inflation. How many investments can you say that you get personal enjoyment from looking at them? Owning an antique car is certainly more enjoyable than owning a piece of paper that says you own shares in company XYZ.

6. Corporate Stock

Corporate stock is a time-tested way  to outpace inflation over long periods of time, survive political and economic turmoil, and potentially provide income to the family. A good example of this is BMW. BMW is based in Germany and founded in 1913. The company survived WW1, WW2, hyperinflation, and a potential liquidation in 1959. This is not to say that all company stocks will be good long term investments, but if chosen properly, this asset class should help sustain a family’s wealth through multiple generations. Part of the reason that company stock outperforms inflation is that companies are able to pass along the inflation to their customers through higher prices. In addition, if the company pays dividends, then the family might benefit from an additional income stream as well.

to outpace inflation over long periods of time, survive political and economic turmoil, and potentially provide income to the family. A good example of this is BMW. BMW is based in Germany and founded in 1913. The company survived WW1, WW2, hyperinflation, and a potential liquidation in 1959. This is not to say that all company stocks will be good long term investments, but if chosen properly, this asset class should help sustain a family’s wealth through multiple generations. Part of the reason that company stock outperforms inflation is that companies are able to pass along the inflation to their customers through higher prices. In addition, if the company pays dividends, then the family might benefit from an additional income stream as well.

7. Timberland

While timberland qualifies as real estate, it has some different characteristics than rental real estate, which are important to note. Timberland’s historica l performance and correlation to other assets, including commercial real estate, is a large part of the attraction of wealthy individuals and families. Also if it is well managed, it can provide long-lasting wealth protection and growth. The historical returns of timberland (according to NCREIF from 1987-2010) are approximately 13.5%. The correlation of timberland to US equities and US bonds is close to zero. This translates to consistent returns not tied to the performance of the stock and bond markets. Timberland also has an uncanny ability to outpace inflation, which tends to be a concern for families with multi-generational wealth. If a family wants to create long-lasting wealth, timberland is a must-have for part of a portfolio.

l performance and correlation to other assets, including commercial real estate, is a large part of the attraction of wealthy individuals and families. Also if it is well managed, it can provide long-lasting wealth protection and growth. The historical returns of timberland (according to NCREIF from 1987-2010) are approximately 13.5%. The correlation of timberland to US equities and US bonds is close to zero. This translates to consistent returns not tied to the performance of the stock and bond markets. Timberland also has an uncanny ability to outpace inflation, which tends to be a concern for families with multi-generational wealth. If a family wants to create long-lasting wealth, timberland is a must-have for part of a portfolio.

8. Farmland

This is another classic asset that wealthy families have invested in over many generations. This also falls under the real estate category, but farmland has certain characteristics which other assets in the list do not have. Just like timberland, farmland is resistant to inflation, has a low correlation to other assets, historically provides decent performance, and if managed well can last generations, but it can also be used for sustainable living if the need arises. Regardless of the political and economic climate, well-maintained farmland can sustain a family as long as necessary. While it is unlikely that a farm is necessary to survive in this technological era, it provides a sense of security to a family, so that if all else goes wrong, there will always be a place that can provide the basics of life.

9. Don’t flaunt it

Both friends and thieves welcome the opportunity to spend someone else’s money. Someone who earns their wealth is much more likely to protect it than someone who inherits it. I have noticed that some extremely wealthy people revert to a façade of someone who is of average wealth in order to avoid scrutiny or targeting. While this might seem extreme, with great wealth comes great responsibility.

10. Use wealth to fund future growth

Entrepreneurs are starting new businesses every day across the country, and one of the biggest challenges is the lack of proper funding to build and grow the business. When a family already has wealth, this can be used to fund startup ventures or invest in other potential ventures. Rather than taking the wealth and investing in a fund or basket of investments, family members should consider taking more of an active role with their investments. Not only does this give them experience in managing their wealth, but it may also provide them additional opportunities to invest in areas that they have a personal interest in.

How can I invest like the wealthy 1%?

This is not an exhaustive list of ways to secure and grow your wealth for future generations. There are many additional ways that wealthy families can extend the use of their wealth. For more information about how this can benefit your family, you can contact us to learn more.

People who have large amounts of wealth have different challenges than the average person. If you have created or inherited a large amount of wealth, and you are thoughtful enough to want to protect it for the future generations of your family, then you will want to consider investments that will last longer than your lifespan. Contact us to learn more about how our Wealth Management services can help you plan for future generations of your family.

About Innovative Advisory Group: Innovative Advisory Group, LLC (IAG), an independent Registered Investment Advisory Firm, is bringing innovation to the wealth management industry by combining both traditional and alternative investments. IAG is unique in that we have an extensive understanding of the regulatory and financial considerations involved with self-directed IRAs and other retirement accounts. IAG advises clients on traditional investments, such as stocks, bonds, and mutual funds, as well as advising clients on alternative investments. IAG has a value-oriented approach to investing, which integrates specialized investment experience with extensive resources.

For more information, you can visit www.innovativewealth.com

About the author: Kirk Chisholm is a Wealth Manager and Principal at Innovative Advisory Group. His roles at IAG are co-chair of the Investment Committee and Head of the Traditional Investment Risk Management Group. His background and areas of focus are portfolio management and investment analysis in both the traditional and non-traditional investment markets. He received a BA degree in Economics from Trinity College in Hartford, CT.

Disclaimer: This article is intended solely for informational purposes only, and in no manner intended to solicit any product or service. The opinions in this article are exclusively of the author(s) and may or may not reflect all those who are employed, either directly or indirectly or affiliated with Innovative Advisory Group, LLC.