If you are like most investors, you probably have not heard of IRA prohibited transactions. Prohibited transactions specifically apply to retirement plans such as self-directed IRAs or 401ks. It is estimated that less than 20% of investors fully understand the flexibility that a self-directed IRA offers, so most IRA account holders won’t have reason to come into contact with this rule. If you do use your retirement plan to invest in alternative investments, then please keep reading.

What is an IRA prohibited transaction?

A prohibited transaction can be described as an improper use of your IRA account assets by a disqualified person. The term prohibited transaction in this case applies to retirement plans such as a self-directed IRA, or 401(k) The IRS defines a prohibited transaction as:

"A prohibited transaction is a transaction between a plan and a disqualified person that is prohibited by law... If you are a disqualified person who takes part in a prohibited transaction, you must pay a tax."

Prohibited transactions can take many forms, but if you keep in mind that prohibited transaction rules are in place to prevent disqualified persons from exerting improper influence on an IRA or 401(k), then it should make it easier to understand.

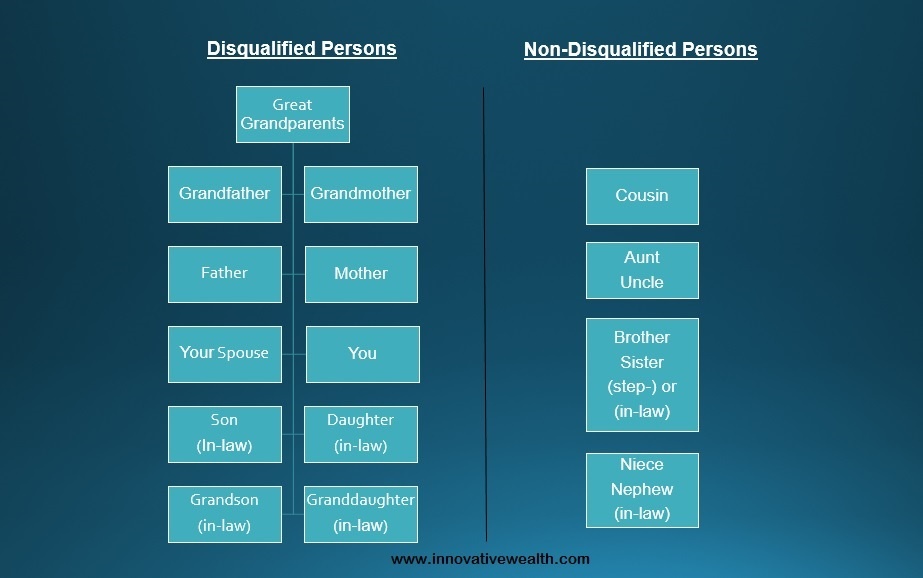

Who is a Disqualified Person?

Here are some transactions that would be considered prohibited:

- a transfer of plan income or assets to, or use of them by or for the benefit of, a disqualified person;

- any act of a fiduciary by which plan income or assets are used for his or her own interest;

- the receipt of consideration by a fiduciary for his or her own account from any party dealing with the plan in a transaction that involves plan income or assets;

- the sale, exchange, or lease of property between a plan and a disqualified person;

- lending money or extending credit between a plan and a disqualified person; and

- furnishing goods, services, or facilities between a plan and a disqualified person.

If you have an IRA or 401(k), you may be scratching your head wondering how this applies to you. This rule actually applies to everyone who has an IRA or 401(k), however the truth is that 95% of IRA account holders will probably never have to worry about this at all. If you choose to invest your retirement account into alternative investments such as real estate, horses, or private company stock should be aware of these rules so they don't violate them causing penalties and taxes to be paid.

What happens if you create a prohibited transaction with your IRA or 401k?

When a prohibited transaction is created, the IRA account involved is treated as if the entire amount was distributed on the first day of the year in which the prohibited transaction occurred. Occasionally this can be corrected if discovered in time, but if it is not corrected, here are some examples of what can happen. When a prohibited transaction takes place the following actions can happen with some more severe penalties if not caught in time:

- The account involved in the prohibited transaction are considered as being distributed on the first day of the year in which the transaction happened.

- The account involved in the prohibited transaction would be considered income for that year, applicable taxes would have to be paid on that income.

- If this transaction occured before the owner of the IRA is 59.5, then early distribution rules would apply. This could include an early distribution penalty of 10%.

- A prohibited transaction tax of 15% would be assessed to all assets involved in the transaction.

- If this prohibited transaction is not caught in time only to be discovered years later, then the owner of the IRA could be assessed penalties, interest on taxes and penalties owed, and late fees. Obviously catching this early is important.

The key point is to not create prohibited transactions. But if one does occur, make sure you address it early enough so as to not incur further penalties. If you are investing in alternative investments with your retirement account, make sure you work with a licensed professional who understands self directed IRAs and the applicable rules. Working with an expert can help you prevent future problems from occurring.

Self directed IRA prohibited transactions that could tax you

These 6 prohibited transactions are the most common ones we see from investors who jumped into self directed IRA without guidance or advice. Hopefully you can learn from their mistakes and keep your self directed IRA money from the taxman until you retire.

Prohibited Transaction #1 - Providing "sweat equity" to your IRA

Most people understand the saying, "the carpenter with a leaky roof" as meaning that professionals may be good at their job, but they are usually too busy to take care of their own problems. Problems that could easily be remedied with their own professional skills. Many real estate investors are accustomed to doing their own handy-work for their investment properties. If you own real estate in your IRA, this will be an issue. You are not allowed to fix the roof of a rental property you own in your self directed IRA. You cannot contribute "sweat equity" into the property.

No benefit can be provided by the owner of an IRA to that IRA. In this case, the owner of the IRA would be providing a benefit to the IRA by fixing the roof. While the owner cannot do the work himself, he could hire a non-disqualified person to fix the roof for him.

Prohibited Transaction # 2 - Personal use of IRA investments

Real estate can be a good way to build a consistent passive income stream. Many investors buy real estate to derive passive income. Despite the disruption in real estate prices during the period of 2005-2011, historically real estate is has been a great hedge against inflation. Some investors use their capital to invest in vacation real estate they can rent out but also use occasionally. The occasional self-use is not allowed with IRA owned real estate.

Let's say you are building your real estate portfolio in your IRA and your mom needs a place to live. Why not have her rent your real estate as a way to shelter income in your IRA? Taking care of dear old mom may sound like a normal thing to do, but you cannot do this with investments held in your IRA. If you own rental property in your IRA, you cannot rent it to you mother. Your mother is a disqualified person in the eyes of the Internal Revenue Code. You cannot rent your real estate to any disqualified person. If your mother needs a place to live, then you might want to consider using taxable funds.

Prohibited Transaction #3 - Death and taxes

I'm sure you have heard the quote by Benjamin Franklin,

"...nothing is certain except death and taxes." - Benjamin Franklin*

Yes both death and taxes are inevitable. If you have money in an IRA, it will be taxed (Roth IRA money gets taxed going in rather than going out). Just accept this premise as it has no legal exception. However some people think they are smarter than the IRS. Let me give you some quick advice. You are not smarter than the IRS. The endless number of tax court cases will prove you wrong.

Some people have suggested that one way to avoid certain retirement plan rules is to place the investment inside a LLC or other legal entity, where the entity is 100% owned by the IRA. While you may think that the activities held inside the IRA may be hidden from the IRS, they are not, and it doesn't change the rules. The same rules are valid whether the investment is held inside or outside a LLC (owned by the IRA). There may be some advantage and disadvantage to using a legal entity to hold investments inside an IRA, but the rules pertaining to prohibited transaction still apply no matter what type of entity you use.

* This quote originated with Christopher Bullock, The Cobler of Preston (1716).

Prohibited Transaction #4 Selling an investment to your IRA

This is by far the most common question:

" If I own real estate, can I put it into my IRA?"

The answer is no. If you own real estate in your name, you cannot put it in your IRA. This would be considered doing business with yourself, which is not allowed. You are considered a disqualified person so this would be a prohibited transaction.

You might think what difference does it make? Think about it this way. At what price do you sell the investment to your IRA? Is there a way to do this objectively without bias to yourself or your IRA? Not really, so it is disallowed.

Prohibited Transaction # 5 - Can I loan myself money?

"Neither a Borrower nor lender be"

- Polonius in William Shakespeare's Hamlet

Using your IRA to loan funds to others can be a successful strategy if done properly. Many people loan money as a secured note backed by real estate, equipment, inventory, or other assets. Some people even lend money as unsecured notes. Many times when an investor runs short on funds for a project or investment, they turn to their IRA as a lender. Unfortunately this is also not allowed since your IRA cannot loan funds to a disqualified person (you). Instead of loaning funds to yourself, consider loaning your IRA funds to other people. This can be an interesting investment strategy if you know what you are doing.

Conclusion

The prohibited transaction rules are important to know and should not be too much of a hindrance to your investing strategy. These rules are clearly defined in the Internal Revenue Code and Retirement Plan Investments FAQs. If you are looking to invest your assets into alternative investments with your retirement plan, make sure you work with a licensed professional legal, tax, or financial advisor. Someone who has experience working on these types of investments. They can help you navigate the hurdles that come into play with alternative investments. If you are looking for financial advice pertaining to alternative investments held in a self directed IRA or 401k, feel free to contact us for you information about our services.

Get our Free Special Report: 9 Common Mistakes Made By Self-Directed IRA Investors.

Innovative Advisory Group is a top provider of self-directed IRA investor education and financial advice. Sign up for this Free Report and learn how we can help you become a better self-directed IRA investor.

About Innovative Advisory Group: Innovative Advisory Group, LLC (IAG), an independent Registered Investment Advisory Firm, is bringing innovation to the wealth management industry by combining both traditional and alternative investments. IAG is unique in that they have an extensive understanding of the regulatory and financial considerations involved with alternative investments held in self directed IRAs and other retirement accounts. IAG advises clients on traditional investments, such as stocks, bonds, and mutual funds, as well as advising clients on alternative investments. IAG has a value-oriented approach to investing, which integrates specialized investment experience with extensive resources.

For more information you can visit: Innovative Advisory Group

About the author: Kirk Chisholm is a Wealth Manager and Principal at Innovative Advisory Group. His roles at IAG are co-chair of the Investment Committee and Head of the Traditional Investment Risk Management Group. His background and areas of focus are portfolio management and investment analysis in both the traditional and alternative investment markets. He received a BA degree in Economics from Trinity College in Hartford, CT.

Disclaimer: This article is intended solely for informational purposes only, and in no manner intended to solicit any product or service. The opinions in this article are exculsively of the author(s) and may or may not reflect all those who are employed, either directly or indirectly or affiliated with Innovative Advisory Group, LLC.